Summary & Key Takeaways

The Story

The EU winter crunch was driven by the interaction of three forces that Snowtrail

tracks through three interconnected products:

- Weather (WRSI): Cold forecast uncertainty created demand risk

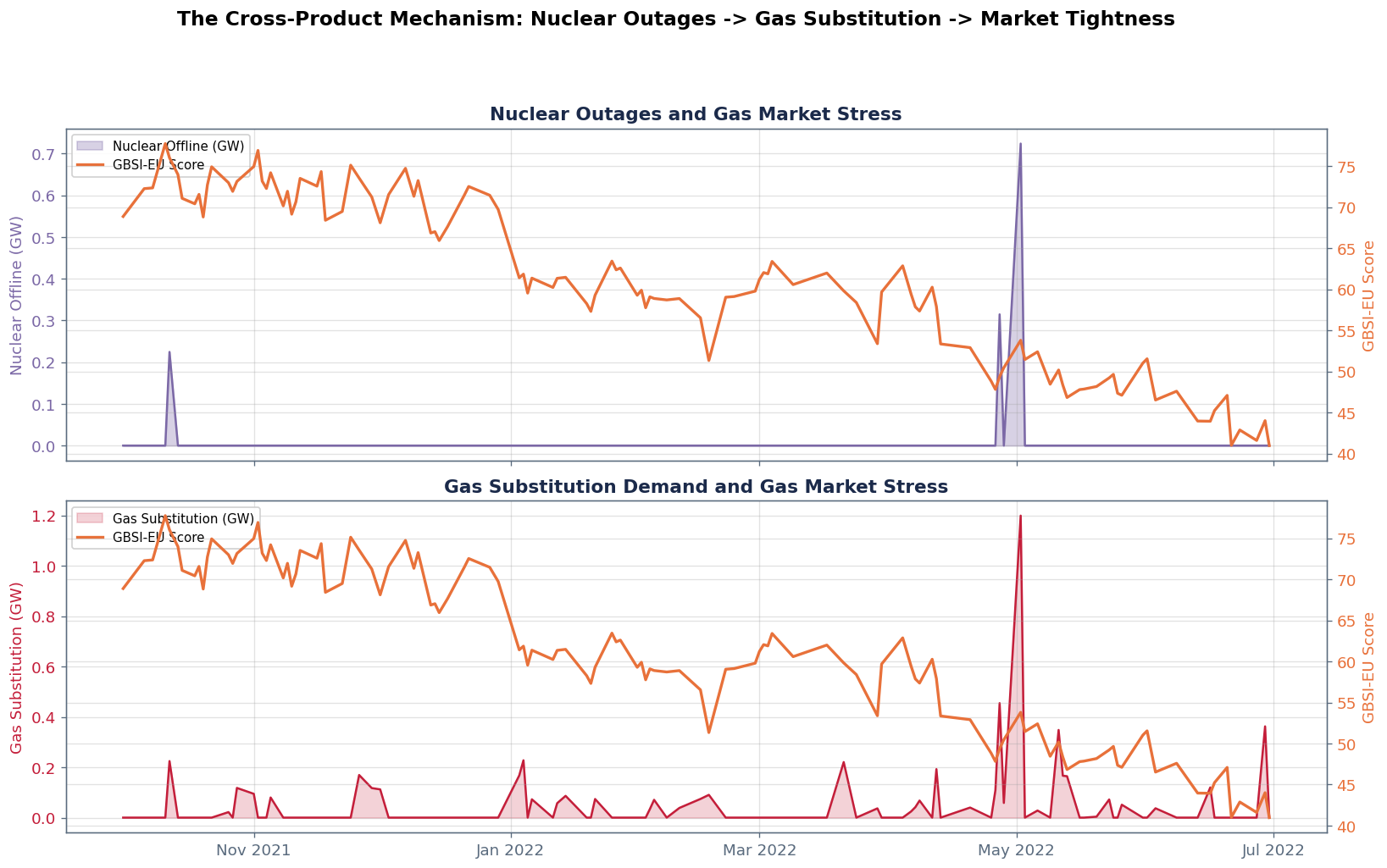

- Nuclear (PEMI): France's nuclear fleet went offline. Gas-fired generation

had to fill the gap, driving gas demand higher

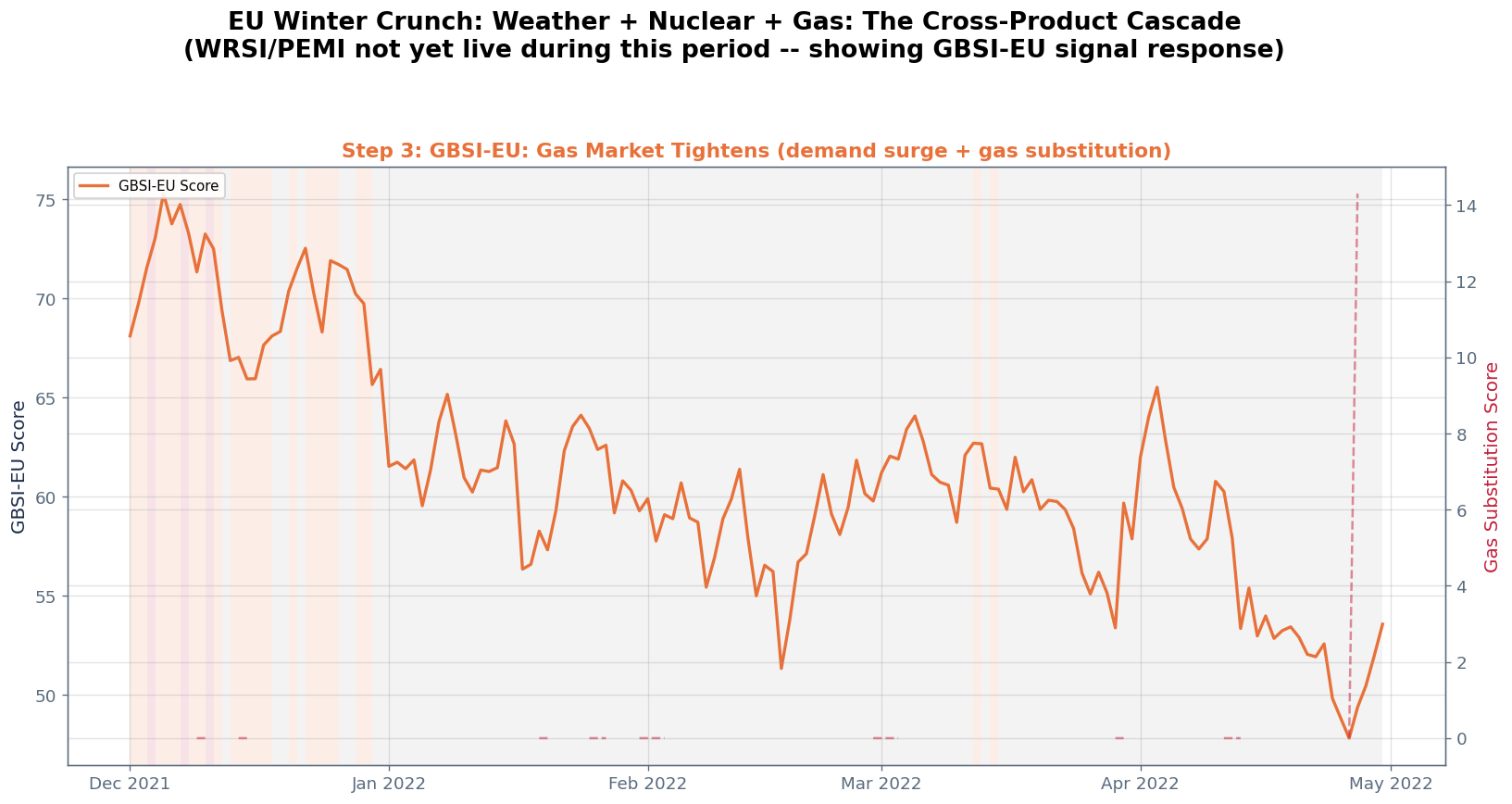

- Gas balance (GBSI-EU): The combination of cold-driven demand and gas substitution

from nuclear outages created compound stress in the gas market

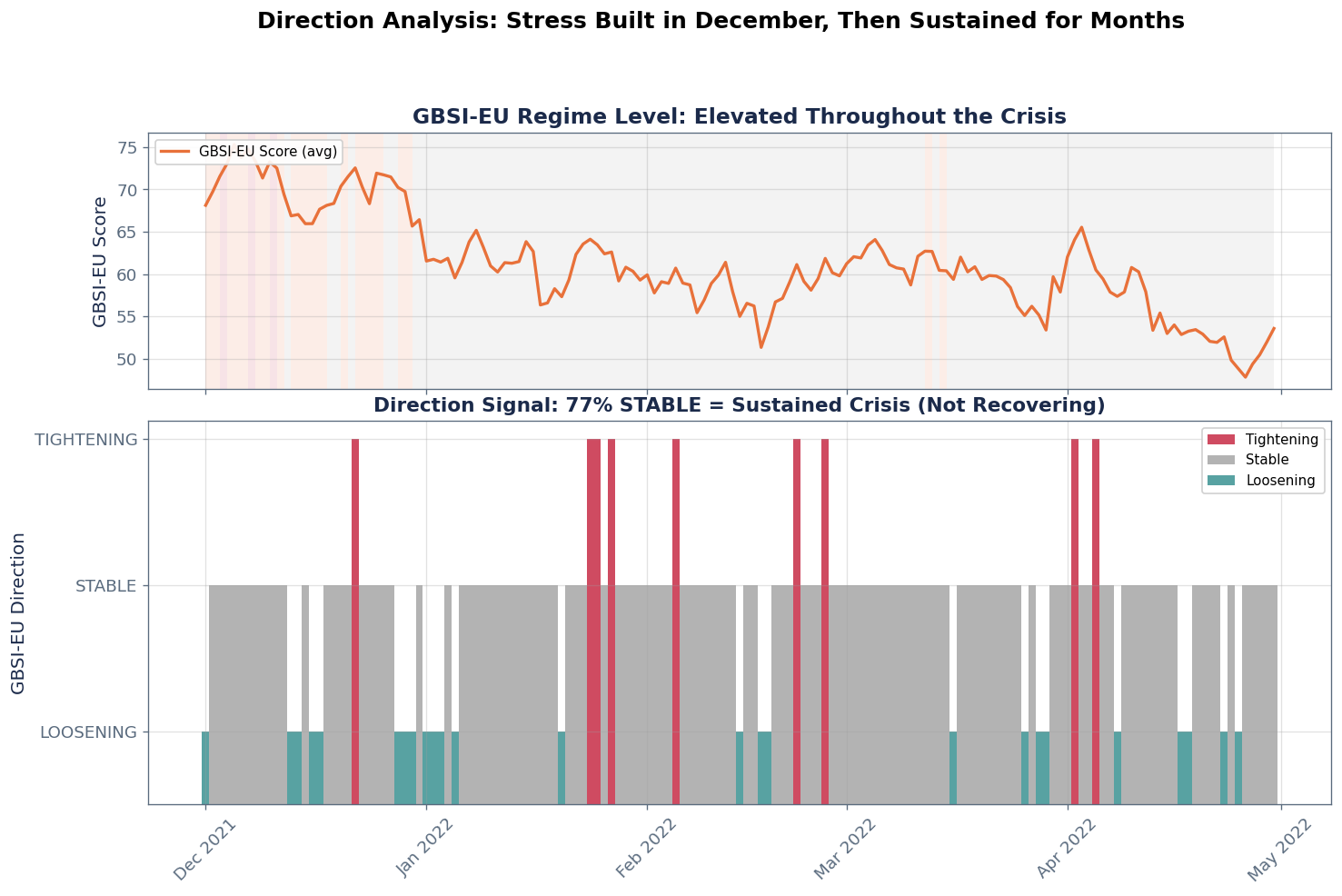

The Direction Signal

A STABLE signal at an elevated baseline is the signature of a sustained crisis. The initial

TIGHTENING in December 2021 (stress building) gave way to months of STABLE direction

(stress plateaued at crisis levels). Occasional LOOSENING never persisted. For position

sizing, this is the difference between a day trade and a multi-month position.

What the Data Shows

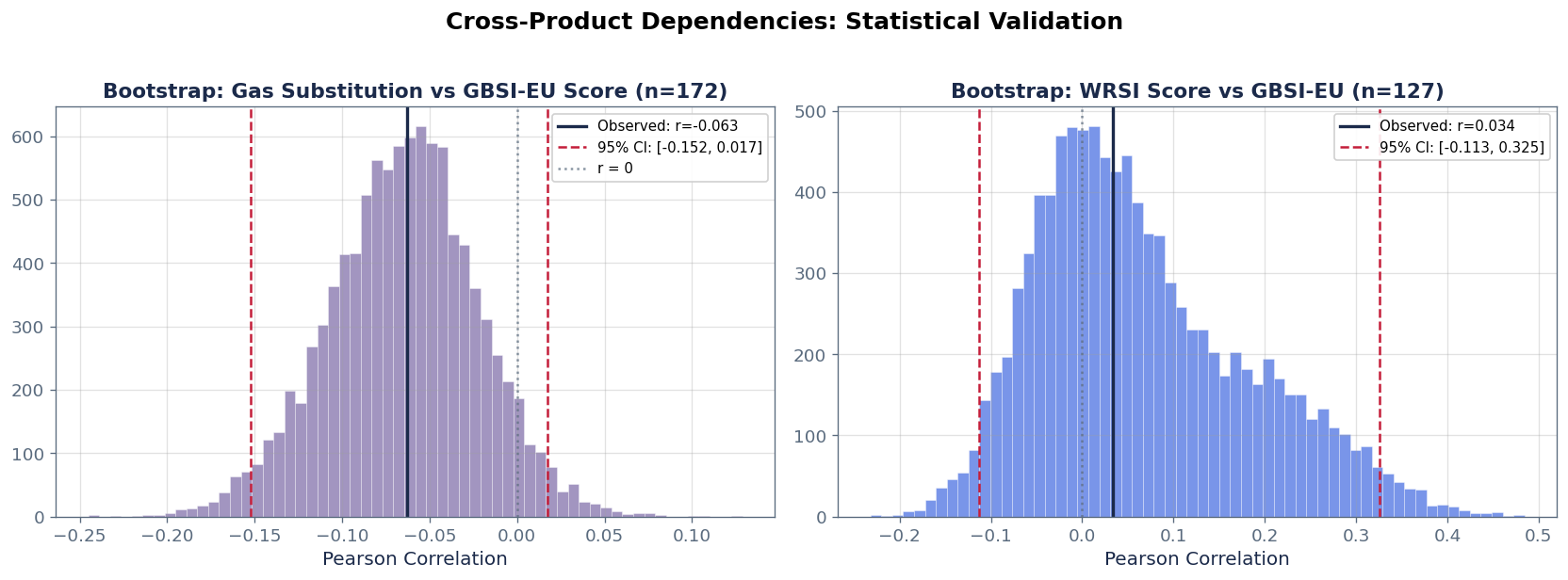

- Gas substitution mechanism: The gas_substitution_score is a structural pillar

within GBSI-EU. Bootstrap correlation with the composite is weak at the daily level

(r~-0.06, CI includes zero), expected because other pillars offset it.

The dependency is structural, not correlational.

- Weather amplification gate did NOT fire: Nuclear outages were so severe that

weather amplification was not needed. This remains the second line of defence for the next crisis

- Direction confirmed sustained stress: 77% STABLE during the crunch

- Three-product cascade: WRSI -> PEMI -> GBSI-EU temporal sequence confirmed

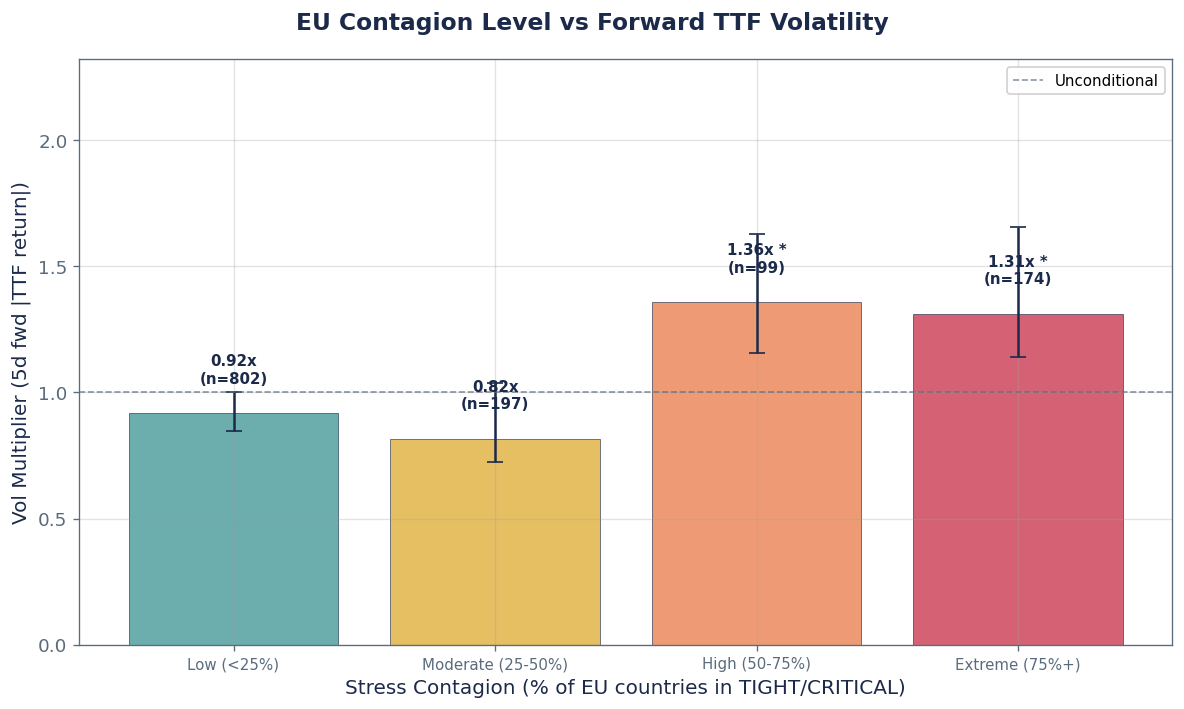

- Contagion is the significant predictor: Individual GBSI-EU regime and direction

do not achieve statistical significance for TTF vol. EU-wide contagion

(% of countries in TIGHT/CRITICAL simultaneously) is the only predictor where

bootstrap CIs exclude 1.0x. This is what distinguishes EU from US gas risk

What a Client Does With This

EU Power/Gas Trading Desk:

- WRSI TRANSITION + PEMI nuclear offline rising = compound risk building. Long TTF,

long power forwards. The cascade gives you one to two weeks of lead time

- GBSI-EU direction = STABLE at elevated levels: do not expect relief. Maintain

long positions. The crisis is not getting worse but it is not going away

- GBSI-EU direction = LOOSENING that does not persist: false relief. Do not cover

longs on a single week of LOOSENING. Wait for consecutive weeks

- PEMI weather amplification gate active = the 2.0x multiplier fires. This is the

highest-conviction trade signal: nuclear moderate + cold extreme = compound crisis

Utility with Gas + Power Exposure:

- WRSI TRANSITION = cold forecast with high uncertainty. Pre-position gas procurement

and power hedges before the cascade reaches GBSI-EU

- PEMI nuclear_offline > 30% = gas-for-power substitution demand rising. Your

gas supply costs will increase even without a cold snap

- STABLE direction at TIGHT/CRITICAL = sustained elevated procurement costs.

Renegotiate supply contracts, activate flexibility clauses

Risk Manager:

- The three-product cascade is a stress-test template: when WRSI + PEMI + GBSI-EU

align, standard VaR underestimates. Apply compound stress scenarios

- Direction persistence (77% STABLE for 5 months) = time-weighted risk is much

larger than point-in-time VaR suggests. Adjust holding period assumptions

- Contagion level is the statistically significant risk metric for TTF: when 50%+

of EU countries are simultaneously stressed, forward TTF vol rises above

unconditional. Use contagion as the regime-conditional VaR input for EU gas

- The gas substitution score is a leading indicator of cross-commodity correlation.

When it rises, gas-power correlation increases. Hedge accordingly

The Bottom Line

Weather risk alone didn't explain the TTF move. Nuclear outages alone didn't

explain it either. It was the compound effect, and the direction signal showed

the worst part: once stress reached crisis levels, it stayed there for months.

STABLE at a high baseline means "do not expect relief."