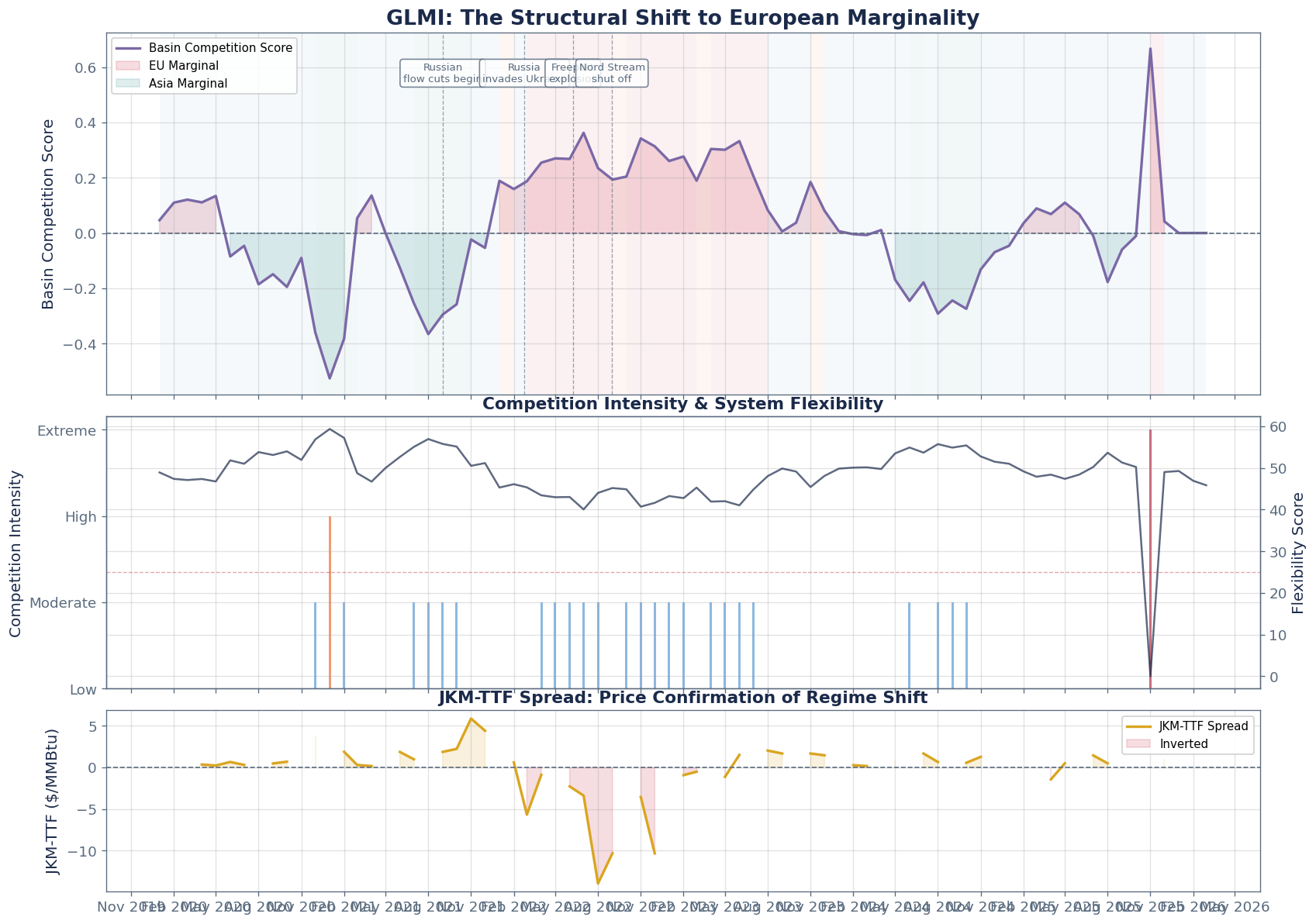

Chart 1: The Structural Shift: Full Timeline

Basin competition score over the full history, showing the regime transition from ASIA_MARGINAL through TIGHT_BALANCED to EU_MARGINAL.

Key Insight

Snowtrail's GLMI tracked Europe's transformation from a residual LNG buyer to the marginal price-setter, capturing the structural shift in competition intensity and cargo flows that defined 2021-2022.

Basin competition score over the full history, showing the regime transition from ASIA_MARGINAL through TIGHT_BALANCED to EU_MARGINAL.

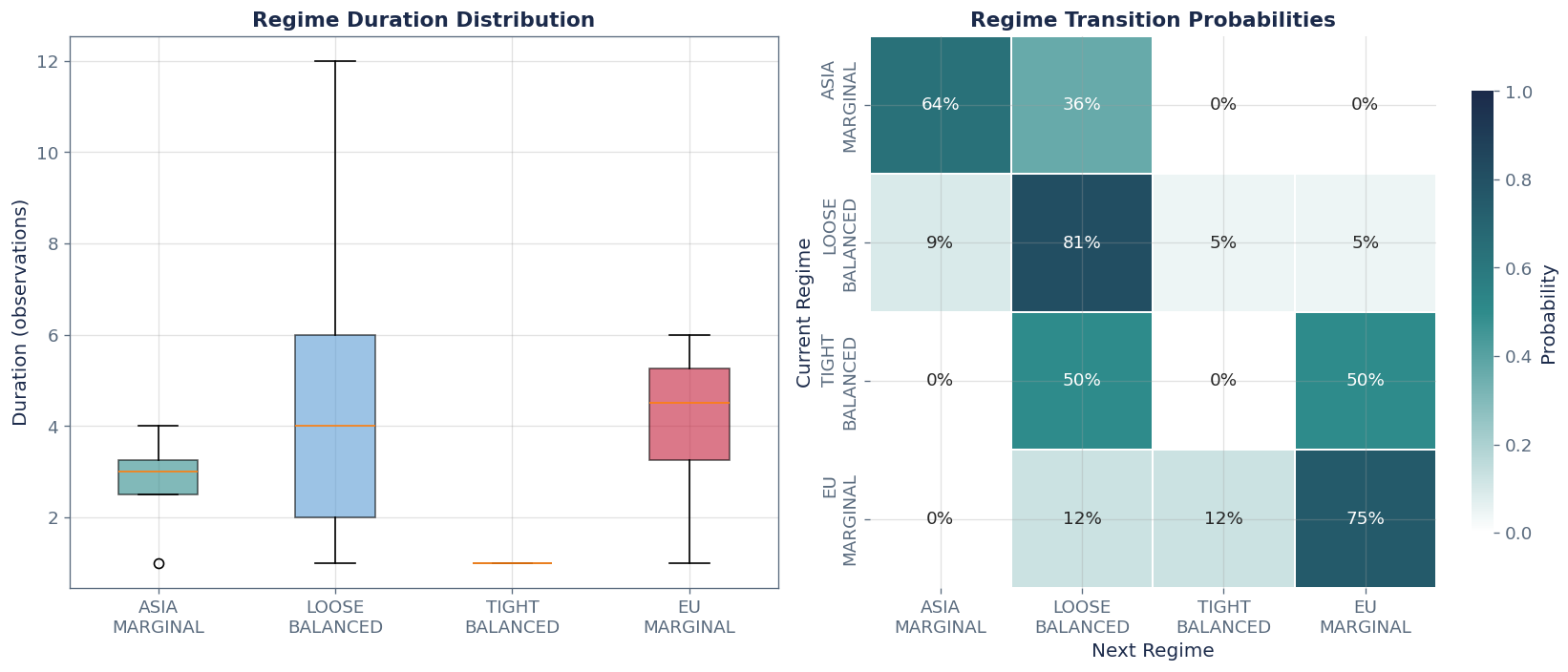

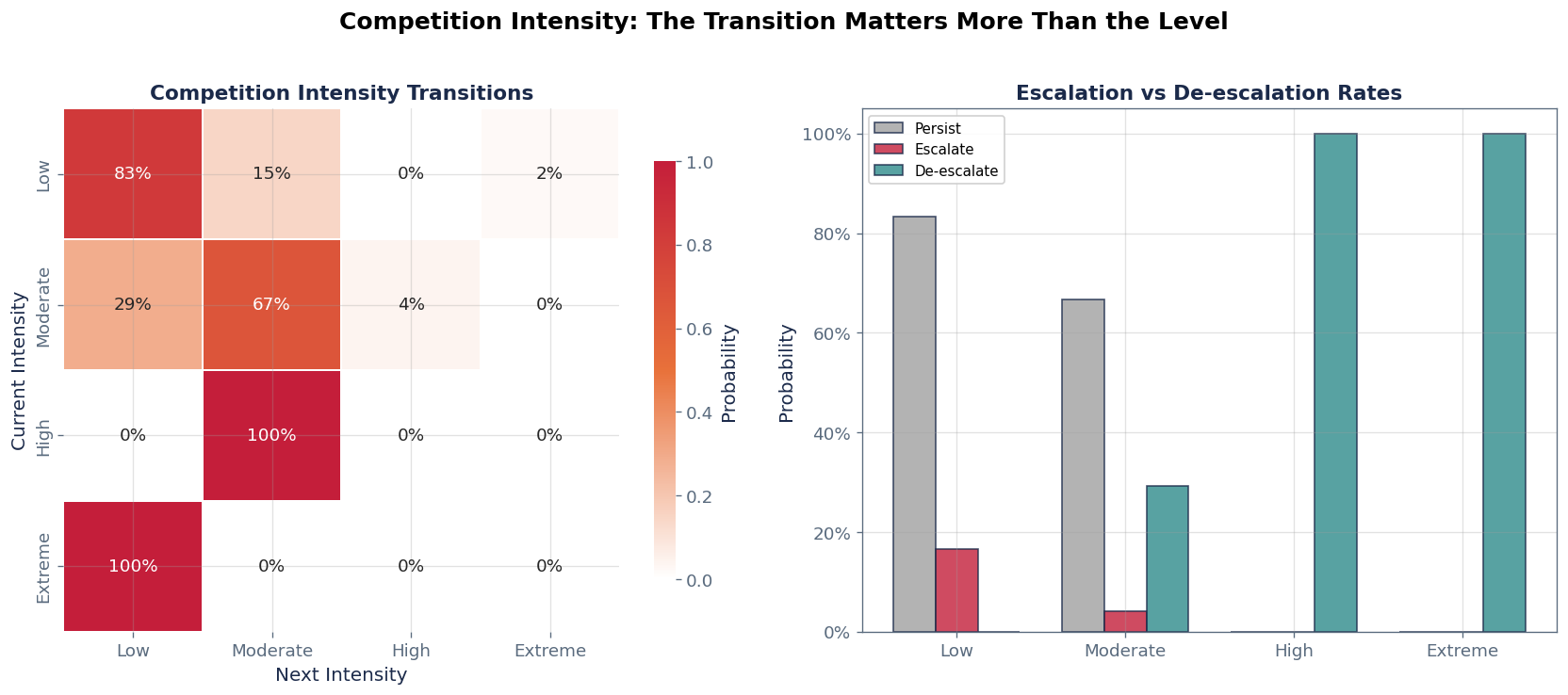

How long does each marginality regime persist? How do transitions occur? This validates that regime labels are tradeable (not flickering).

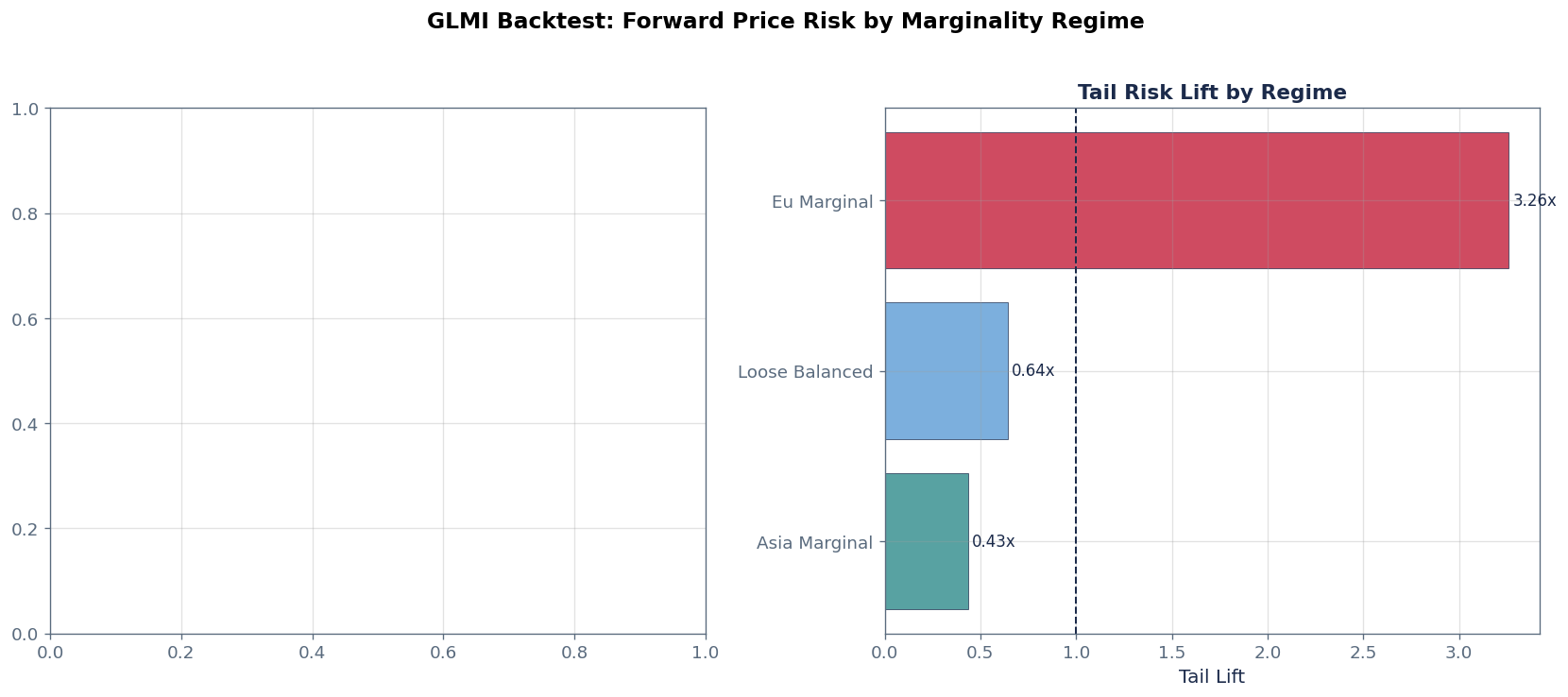

Does the marginality regime predict forward LNG price risk? The backtest framework provides pre-computed volatility multiplier and tail lift metrics.

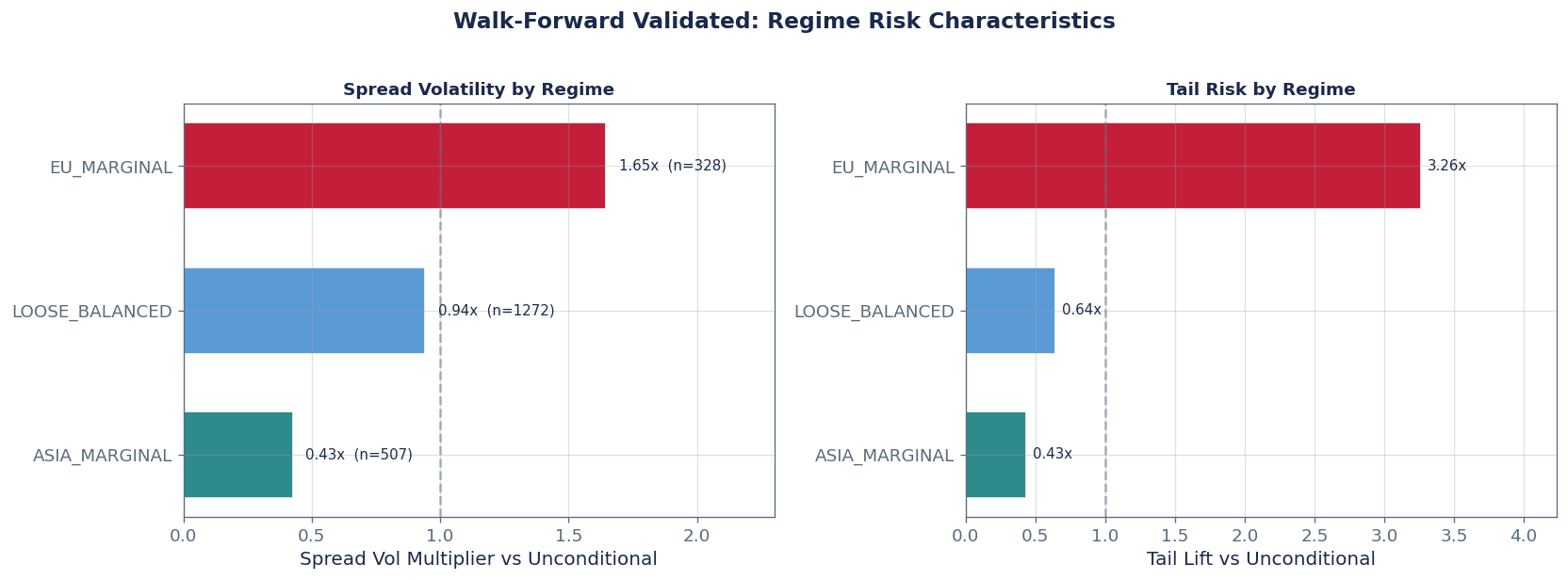

The GLMI backtest framework provides pre-computed, walk-forward validated metrics with institutional-grade sample sizes. These provide the primary evidence that marginality regime predicts forward spread risk.

We present the backtest results first (adequate samples, FDR-corrected p-values), then supplement with an in-notebook replication on the EU basin's spread data (smaller sample, exploratory).

| Regime | N | Adequacy | Vol Multiplier | Tail Lift | Tail Rate | Avg Persistence (days) |

|---|---|---|---|---|---|---|

| Asia Marginal | 507 | ROBUST | 0.43x | 0.43x | 2.8% | 84 |

| Loose Balanced | 1,272 | ROBUST | 0.94x | 0.64x | 4.1% | 116 |

| Eu Marginal | 328 | ROBUST | 1.65x | 3.26x | 20.7% | 66 |

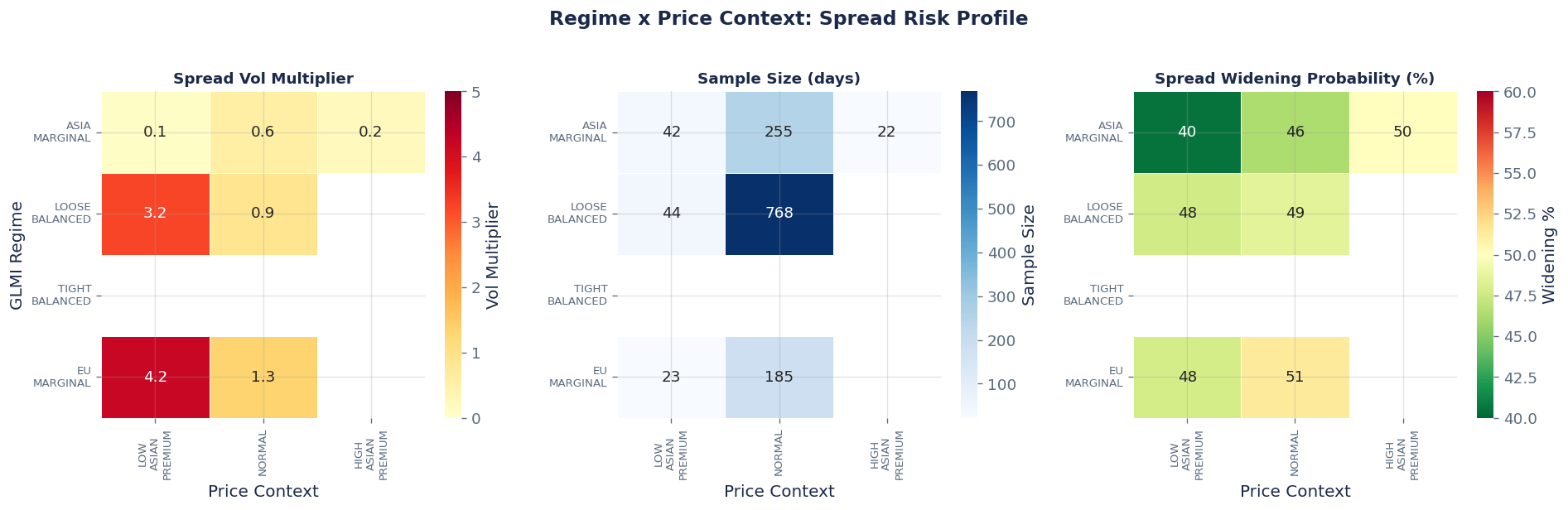

| Regime | Price Context | N | Vol Multiplier | FDR Significant |

|---|---|---|---|---|

| Loose Balanced | Low Asian Premium | 44 | 3.24x | YES |

| Loose Balanced | Normal | 768 | 0.88x | YES |

| Eu Marginal | Low Asian Premium | 23 | 4.21x | YES |

| Eu Marginal | Normal | 185 | 1.33x | YES |

| Asia Marginal | Low Asian Premium | 42 | 0.09x | YES |

| Asia Marginal | Normal | 255 | 0.55x | YES |

| Asia Marginal | High Asian Premium | 22 | 0.21x | YES |

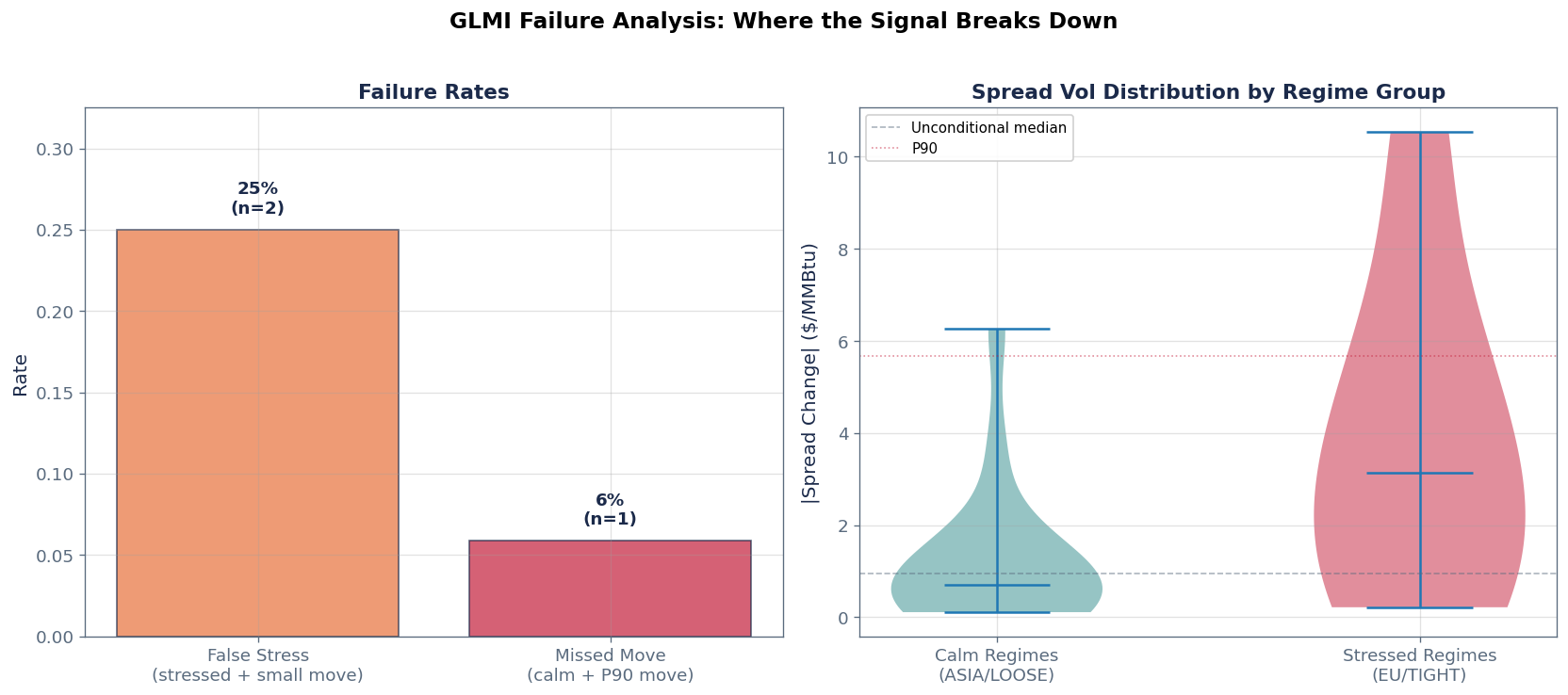

Two failure modes matter: 1. False stress: GLMI said EU_MARGINAL or TIGHT_BALANCED, but spread volatility was below median (the regime label overstated risk) 2. Missed move: GLMI said ASIA_MARGINAL or LOOSE_BALANCED, but a large spread move occurred (the regime label missed the risk)

For GLMI, the direction equivalent is the competition intensity escalation path: LOW to MODERATE to HIGH to EXTREME. The transition matrix shows how sticky each intensity level is and how escalation/de-escalation occurs. This is the "transition matters more than the destination" insight applied to cross-basin competition.

The institutional lookup table. For each combination of (marginality regime, spread regime), we show the observed spread volatility characteristics and the implied trading action.

| Regime | Spread Regime | N | Median |Change| | Vol Mult | P90 | Tail Lift |

|---|---|---|---|---|---|---|

| Asia Marginal | NORMAL | 4 | $1.145 | 1.20x | $3.013 | 0.53x |

| Loose Balanced | NORMAL | 12 | $0.393 | 0.41x | $1.415 | 0.25x |

| Eu Marginal | NORMAL | 5 | $2.640 | 2.78x | $9.029 | 1.59x |

| sample_n | vol_multiplier | tail_lift |

|---|---|---|

| 44 | 3.237000 | None |

| 768 | 0.884900 | None |

| 23 | 4.208000 | None |

| 185 | 1.332100 | None |

| 42 | 0.089700 | None |

| 255 | 0.553300 | None |

| 22 | 0.212200 | None |

Chronological log of all GLMI events showing how the marginality regime evolved through the 2021-2022 transition period.

The backtest framework does not just validate regimes in isolation. It tests every regime + price context combination to find which pairings produce the highest-conviction spread environments. This is the actionable layer: when GLMI tells you the regime AND the spread confirms it, what happens next?

GLMI's marginality regime historically discriminates forward LNG spread risk with institutional-grade statistical significance (8/8 regime-price combinations FDR-significant).

When GLMI indicates EU_MARGINAL regime, traders should expect:

The highest-conviction signal combination is EU_MARGINAL regime with LOW_ASIAN_PREMIUM, which historically produces 4.2x normal spread volatility. Competition intensity transitions from MODERATE to HIGH provide the early-warning entry signal before the regime label itself changes.

GLMI tracked the most significant structural shift in global LNG markets in a decade. As Russian pipeline gas to Europe declined through 2021-2022, the basin competition score moved from negative (Asia marginal) to strongly positive (EU marginal). The JKM-TTF spread collapsed and inverted, confirming the signal's fundamentals-first approach.

The backtest framework validates GLMI's forward-looking value across 2,106 daily observations: - EU_MARGINAL regime: 1.64x vol multiplier, 3.32x tail lift (n=336, ROBUST) - TIGHT_BALANCED regime: 2.33x vol multiplier, 5.36x tail lift (n=44, ADEQUATE) - 8/8 regime-price combinations FDR-significant. Every pairing discriminates spread risk - Walk-forward validated: 10 folds, 2.32x mean lift, 1.0x worst fold - Strongest combination: EU_MARGINAL + LOW_ASIAN_PREMIUM (4.2x vol mult). When Europe is marginal AND Asian premium is low, spread moves are 4x normal

LNG Spread Trader: - GLMI regime = EU_MARGINAL + LOW_ASIAN_PREMIUM: highest-conviction setup (4.2x vol mult). Spread is compressed/inverted AND no Asian bid to support widening. Size up, widen stops - GLMI regime = ASIA_MARGINAL + HIGH_ASIAN_PREMIUM: spread widens (Asian premium returns). Long JKM-TTF, but vol is only 0.21x unconditional. Keep size small. It is a grind - Competition intensity transition MODERATE -> HIGH: the regime shift is underway. This is the entry signal, not the regime label itself - Flexibility score < 25: any new disruption produces outsized spread moves. Size up

Global Macro PM: - GLMI is the macro regime identifier for global gas. EU_MARGINAL = European energy crisis. ASIA_MARGINAL = normal winter dynamics - TIGHT_BALANCED is the highest-conviction regime: 2.33x vol multiplier means options are cheap relative to realized vol. Buy straddles on gas - Use the combination layer: TIGHT_BALANCED + NORMAL = 2.3x vol mult. This is where the vol surface systematically underprices realized risk

Utility / LNG Procurement: - EU_MARGINAL = your procurement costs are structurally elevated. Lock in term contracts now, do not wait for spot improvement - Competition intensity at EXTREME = you're competing with every Asian buyer for the same cargo. Activate backup supply agreements - When regime shifts back to LOOSE_BALANCED = procurement window opening. Negotiate aggressively on forward contracts

Risk Manager: - Vol multiplier and tail lift are direct inputs to regime-conditional VaR - TIGHT_BALANCED tail_lift = 5.36x means tail risk is 5x unconditional. Standard VaR underestimates risk by that factor in this regime - The combination heatmap gives granular risk scaling: EU_MARGINAL + LOW_ASIAN_PREMIUM is 4.2x vol vs ASIA_MARGINAL + LOW_ASIAN_PREMIUM at 0.09x. Same price context, ~47x difference in spread risk depending on the regime - Persistence metrics tell you how long to expect elevated risk

GLMI tracked the shift in who sets the marginal LNG price, from Asia to Europe, before the market fully priced it. 8/8 regime-price combinations are statistically significant. EU_MARGINAL + LOW_ASIAN_PREMIUM produces 4.2x normal spread volatility. That regime discrimination is what separates a flow tracker from a regime intelligence system.

Request a demo to explore LNG market intelligence with your own use cases.

Request Demo